On 1 July 2019, the Fair Work Commission increased the national minimum wage in Australia by 3%. While this may not sound like that big of a deal, it could have a significant impact on cash flow for many SMEs.

In this post, we’ll look at the details and explain how to ensure your business has adequate cash flow in the face of this change.

The Highlights

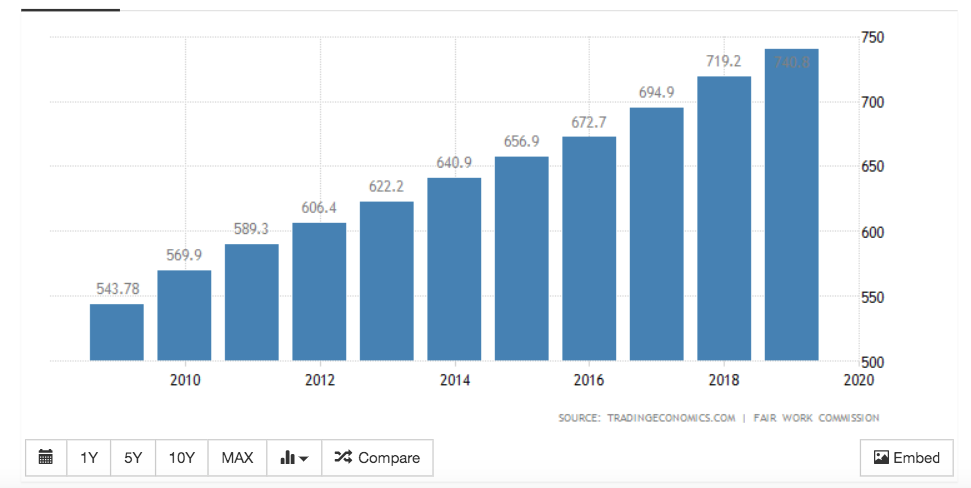

“The minimum wage from July 1 will be $19.49 an hour, or $740.80 a week for full-time workers,” explains Sydney-based business reporter, Stephanie Chalmers in ABC News. “The Fair Work decision affects around 2.2 million workers on the minimum wage or modern awards.”

This is up from $719.20 per week one year ago in 2018. And considering how minimum wage in Australia continues to steadily increase, this is likely to rise in upcoming years. This graph from Trading Economics of the Australia weekly minimum weekly wage over the years helps put things into perspective.

Designed to increase the wages of employees throughout the country and improve their living standards, it’s a welcome change for low paid workers. It will help this segment of the workforce provide a better life for their families and live more comfortably. So in that regard, it’s positive.

However, these pros aren’t without their cons for employers.

The Downside for SMEs

Unfortunately, the minimum wage increase can create potential hardships for many SMEs that employ these workers and put a strain on cash flow. A recent article from the Recruitment, Consulting and Staffing Association (RCSA) examines the situation and mentions the impact it can have on the labour sector.

In it, they quote Scottish Pacific’s head of debtor finance, Wayne Smith, who said, “An extra 56 cents an hour to $19.49 may not seem like much, but labour hire and recruitment businesses have dozens, sometimes hundreds, of temporary staff on their books and the minimum wage increase could impact on both their margin and their cash flow.”

Money that could go to cash flow to buy goods and equipment, cover operating expenses and expand a business must now be spent on increasing the wages for minimum wage employees. For companies where cash flow was already lean to begin with, this is a real concern.

And while the article from the RCSA applies to SMEs in the staffing/recruiting industry, the minimum wage spike impacts far more companies than that. In fact, any business that employs minimum wage workers will feel the impact.

If your company falls into this category, it’s important to look for other ways to improve your cash flow. Here are some ways to go about that.

Short Payment Terms

A good place to start is to reduce the length of payment terms with your clients. While this won’t always be a realistic possibility for every business, and invoices are more likely to go past due, you’re still more likely to receive your money quicker than if you had longer payment terms.

A study by online accounting software company Xero found:

- 1 week payment terms get settled in about 2 weeks

- 2 week payment terms get settled in 2-3 weeks

- 3 or 4 week payment terms get settled in about a month

So keep this in mind when negotiating a payment structure with future clients or amending payment terms with existing ones. If you have the leverage to dictate payments, it can take a lot of stress off of you and boost cash flow.

Stay On Top of Outstanding Invoices

Late payments are an ongoing problem for more than half of SMEs. In fact, research has found that between July 2017 to July 2018, 53% of smaller companies were paid later than the agreed terms by larger organisations, with the average invoice being late by 23 days. The true cost of late payments can be detrimental to the business.

Experts estimate that this equaled $115 billion in late payments. But if those invoices had been paid on time, small businesses would have had an additional $7 billion in working capital.

These numbers show just how big of an impact late payments can have and why it’s so crucial to stay on top of outstanding invoices. This starts by taking steps to improve debtor management so that you’re able to efficiently track what’s owed to you and when.

The RCSA recommends asking clients for down payments or partial payments on big projects where there’s a lot of money involved. This ensures you have at least a portion of payment right off the bat without having to wait for several weeks or even months for the full amount.

You should also be quick to remind clients that they owe you money once the invoice deadline has passed. The last thing you want to do is wait a week before following up. Instead, send a friendly reminder through email. And if you don’t get a response, pick up the phone and call.

It may not always be pleasant conversation to have, but it’s vital for maintaining steady cash flow and keeping your business afloat.

Look Beyond Bank Loans

Traditional property secured loans from banks are becoming harder and harder to obtain. Increased lending standards due to the Royal Commission and the current property market downturn have resulted in banks being more selective about who they give money to. In turn, many business owners are exploring financing alternatives that don’t involve using property as collateral.

For instance, peer-to-peer lending, short-term loans and equipment financing are becoming popular choices that can potentially supply you with the cash flow needed as you adapt to Australia’s minimum wage increase.

Consider Invoice Finance Solutions

Another option that’s grown by leaps and bounds is invoice finance or debtor finance where you borrow against the money owed to you from clients. With this arrangement, you submit unpaid invoices to a lender. Once approved (this typically happens within 24 hours), you will be paid up to 95% of the value, minus any fees. You then receive the remaining 5% once your client pays the invoice in full.

There are comprehensive options where the lender assumes responsibility for debt collections, freeing up your time to focus on other areas of your business. Or if you have an in-house team and don’t wish to disclose the fact that you’re seeking financing, you can still handle the collections process yourself.

Debtor finance provides an effective way to leverage outstanding invoices and put them to work in order to improve cash flow. The best part is that you’re not reliant upon funding from traditional bank loans — something that’s become more tenuous in recent years.

And with this change implemented by the Fair Work Commission, it can be a potential game changer for SMEs who are struggling. “It’s not always easy to simply pass on the minimum wage increase to their own customers, some may need to absorb an element of the additional cost themselves,” adds Wayne Smith. “Invoice finance can help them deal with this cash flow challenge.”

Getting your Cash Flow Under Control

Australia’s minimum wage increase is certainly good news for low paid workers who are looking to make a better living. However, it does create an obstacle for many SMEs, especially those who are already facing cash flow issues.

Fortunately, there are several viable solutions available that can meet a variety of needs. To learn more about your business finance options, contact Scottish Pacific today.

How big of a strain has the minimum wage increase put on your company’s cash flow? Give us a call to discuss on 1300 207 345 or click here for us to check in