Six-month revenue projections forecast by Australia’s SMEs highlight the sector’s resilience.

Despite fewer than one in 20 Victorian small businesses envisaging revenue growth, Western Australia’s forecasts held up strongly, NSW expectations were not really dampened by the pandemic and Queensland remains reasonably buoyant.

All things considered, SME Growth Index 2021 revenue forecasts for SMEs were less “doom and gloom” than might be expected, although this round of research did record a lowest ever all-respondent positive growth average of +0.1%.

This round also recorded the widest range of positive growth forecasts and the tightest range of negative growth forecasts.

In the midst of Australia’s first recession in 30 years, only 47% of small businesses are expecting revenue growth. Almost three in 10 SMEs forecast unchanged revenue, with around a quarter forecasting a revenue drop through to April 2021. These results mark a record low number of SMEs with positive revenue growth aspirations, the previous low being 48.4% in H2 2017.

Perhaps more surprisingly, the number of SMEs forecasting a revenue decline has moved only one percentage point, to 23.8%, since the last research round in March 2020, despite an immensely challenging past six months for the small business sector.

The SME Growth Index support the premise that targeted government stimulus measures such as JobKeeper have created scaffolding for those SMEs who were already facing the greatest financial difficulty.

It is the other end of the spectrum – high growth SMEs – who have had their revenue expectations reined in by the pandemic. Those expecting revenue to grow are forecasting an +3.3% average result, with the widest ever range reported (+1.0% to +8.8%).

Those expecting their revenue to fall are forecasting an average -6.2% revenue decrease.

Three out of 10 SMEs (29.2%) forecast no change in enterprise revenue over the coming six months, marking a record high proportion of “no change” SMEs above the previous peak of 28.1% in H2 2017.

SMEs’ perception of their own business phase clearly reveals where the pandemic has negatively impacted sentiment. For the first time ever, there are more SMEs self-identifying as being in a stable business phase (33.6%) compared to those in an outright growth phase (32.2%).

One in 10 businesses are in consolidation phase, similar to last round; one in 10 are start-ups and 13.3% identify as declining – a record high above the historical peak of 12.3% in H1 2018.

It will be interesting to see whether this round’s SME revenue forecast was kept artificially high because the Federal Government’s stimulus measures were still in place, with many SMEs able to “keep the lights on” but showing lukewarm enthusiasm about investing significantly in their businesses.

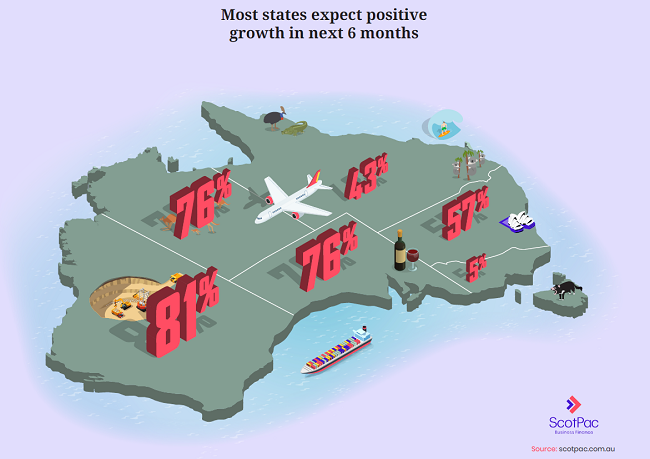

Mainland state revenue expectations

The SME Growth Index found massive variance in revenue forecasts by state and it is likely that this will create an uneven recovery nationally.

NSW:

57% of SMEs expect positive growth

13.5% negative growth

29.5% no change

VIC:

4.6% positive growth

69.1% negative growth

26.3% no change

QLD:

42.7% positive growth

8.9% negative growth

48.4% no change

WA:

80.7% positive growth

3.5% negative growth

15.8% no change

SA/NT:

76.3% positive growth

11.3% negative growth

12.5% no change

It must be noted that SME respondents were polled during September and early October 2020 – a time when Victoria was operating under one of the strictest COVID-19 lockdowns in the world.

The growth expectations of Victorian business owners may quickly improve with the continued easing of restrictions.

Those few Victorian SMEs (4.6%) predicting positive growth expect to bounce back well, with an average 12% revenue growth forecast. But the seven out of 10 Victorian SMEs expecting revenue decline have forecast an 8% average decline.

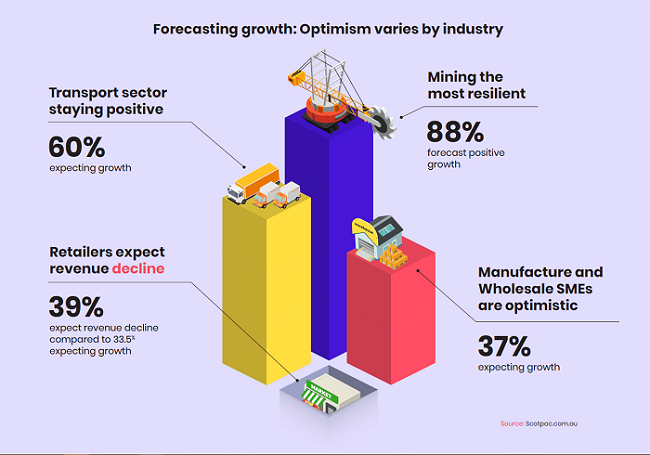

Two-speed economy on show

Of the major industries analysed for the SME Growth Index the mining sector has been relatively unscathed and is most optimistic for the future. The transport industry also shows optimism.

Mining:

87.9% expect positive growth (average growth forecast of 8%)

7.7% forecast a decline (by on average -0.6%)

Transport:

60.2% expect positive growth (3.4% average)

12.2% expecting revenue decline (-2.1% average)

Manufacturing:

37.1% forecast positive growth (of just 1.2%)

29.3% expecting decline (-3.8% average)

Wholesale:

37% expect positive growth (average of 2% growth)

31.5% expecting revenue decline (average -2.5%).

Retail:

33.5% forecast positive growth (of 1.7% on average)

38.7% expecting revenue decline (by a more substantial -4.9%)

It is notable that the retail SME sector is very evenly split between those expecting revenue to grow, decline or remain steady.

These statistics tell a story consistent with separate ScotPac conducted for five months from April to October 2020. This working capital research, across key industry sectors, found that business turnover remained stable during the pandemic, supported by various payment deferral programs and government stimulus initiatives.

With insolvencies down 60% compared to the previous year, businesses were drawing down less money from their funding facilities, and instead many were using the cash harvested from government initiatives to keep their businesses running.

During this five-month period, businesses were paying their peers more quickly – average payment times dropped from 52 to 49 days from April to October.

In October, for the first month since July, Victorian SMEs reported improvement in sales volume across all the key industries analysed.

Transport has been the big winner from COVID-19 due to a surge in e-commence; in Victoria, ScotPac’s working capital research recorded an increase in sales for the transport sector, with a boom in online shopping during the state’s prolonged to stage 4 restrictions.

Manufacturing and wholesale industries saw an immediate impact in sales volume at the start of the pandemic, with signs of recovery during June and July followed by another decline in August and September during Victoria’s stage 4 lockdown.

Previous rounds of the Index highlighted the fact that SME revenue growth targets were precarious, as shown by the range of forecasts expanding and more and more forecasts at the extremes of positive and negative. A summer of bushfires followed by the pandemic pushed many over the edge.

Fortunately, SMEs have weathered what they believe is the worst of the crisis and are now preparing for “COVID normal” as current trading conditions appear here to stay for the short to medium term.