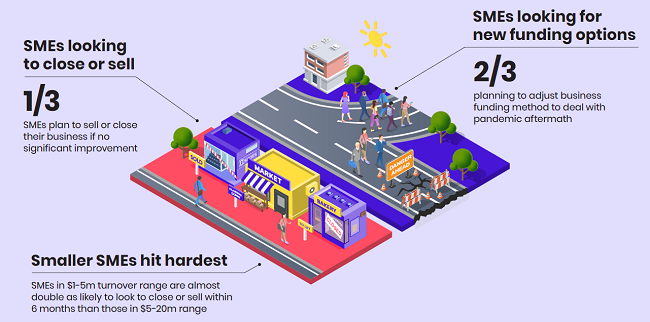

Almost one in three SMEs (31%) indicate that without a significant improvement in trading conditions they may sell or close their business – some immediately, the majority plan to make this decision within three to six months.

This is a stark picture, due to the impact of the COVID-19 recession. However, it’s important to note that the SME Growth Index research took place over a four-week period in September and October, when Victoria was still in lockdown.

So this statistic gives a point-in-time view and is not necessarily a “doom and gloom scenario”, given that trading conditions in November have been improving.

It does, however, serve as a stark indication of the precarious position and potential pain for the small business sector if there was another major state lockdown or significant border closures.

East & Partners Head of Markets Analysis Martin Smith said the one in three SMEs looking to sell or close their business without significant improvement equated to approximately 88,000 businesses around Australia in the $1-20m annual revenue bracket, with about 50,000 of these businesses looking to sell and more than 37,000 looking to close.

The results indicate that the smaller the business, the more severe the impact of the pandemic on their long-term strategic objectives and solvency.

Two out of every five smaller sized SMEs ($1-5m turnover) say they are looking to sell or close by April 2021 unless conditions markedly improve.

Almost one in four larger SMEs ($5-20m turnover) are in the same boat.

Only half (54%) of all the small businesses polled say they are not looking to sell or close due to the impact of the pandemic.

Closing or selling – industry breakdown

There is significant variance by major industry sector: retail has been hardest hit, with manufacturing and wholesale SMEs also heavily impacted. Transport and business services have been resilient, while small businesses in the mining sector have been relatively unaffected.

This indicates a K-shaped recovery taking place, where different sectors recover at different rates, and this is likely to continue until a widely effective vaccine is found and a vaccination program is in place.

- Only 9% of retailers polled are definitely not making plans to close or sell if conditions don’t improve dramatically. More than one in three (34.2%) say they may close, with a similar proportion (31%) planning to sell and almost as many (25.8%) were unsure of what they’d do.

- For manufacturing SMEs, without significant improvement 17.1% would be looking to close, 24.4% to sell, with 18% unsure.

- Transport sector SMEs indicated 3.1% would look to close, 9.2% to sell, with 14.3% unsure.

- Nine out of 10 mining SMEs indicated they would continue in their business even if conditions did not significantly improve.

- A quarter of wholesale businesses were looking to sell, with one in 8 looking to close and a similar proportion unsure of their next steps.

Closing or selling – major state variance

Western Australia and Queensland, who have been under some political pressure for their strict border controls, are home to the small business sectors most confident about not having to close or sell their business.

- For Queensland SMEs, 68.9% felt that even if conditions didn’t significantly improve they would carry on, with only 7.6% saying they could close and 14.7% considering selling.

- For WA, 71.9% of SMEs were confident about staying on, with 5.8% eying closure and 14.6% looking to sell.

- Victoria, hardest hit, was the only state where more than half its SMEs (53.7%) were looking to sell or close – 29.5% listed closing, with 24.2% looking to sell, making Victoria also the only state with a higher sell than close percentage. Only 20% of this state’s SMEs had no plans to sell or close. Victoria had 26.3% of SMEs unsure of what they’d do: two to three times the rate of indecision found in the other states.

- NSW small businesses are much more confident – only 8.8% flagged closing, 18.9% selling and 60.1% had no plans to do either.

- NB – the cohort of South Australian SMEs was too small to allow for meaningful state breakdown on this question.

COVID-19 and stimulus impact on SME borrowing

This round, the SME Growth Index looked at the impact of the pandemic on SME borrowing demand.

More than half the SME sector (56.4%) experienced no significant change in borrowing demand. This figure was split evenly between those who said they relied on government stimulus (28.4%) and those who didn’t require the stimulus (28%).

One in five SMEs reported their funding needs increased in the short-term, with a further 6.6% preparing for an indefinite increase in credit demand.

Only one in 10 SMEs had decreased borrowing demand as a direct result of the pandemic.

SMEs in the midst of the COVID crisis were looking for new answers to perennial funding problems. During the pandemic, one in 12 small businesses (7.7%) added non-bank funding facilities to deal with the impact of the COVID-19 shutdown and subsequent supply chain and revenue issues.

What happens after March 2021?

Business owners were asked what funding adjustments they’d make in response to stimulus measures ending in Q1 2021.

The results point to a significant shakeup within Australia’s small business funding sector.

Nearly two thirds of SMEs (61.8%) are planning to reassess the way they fund their business.

Almost a quarter (22.8%) also plan to reassess their actual funding provider. This was more marked in the $5-20m SME category (31.9% looking to reassess provider) compared to the smaller $1-5m revenue SMEs (14.8%).

It is also notable that 12.3% of SMEs plan to add non-bank funding facilities to cope with their cash flow needs once all the projected Federal Government stimulus initiatives end.

For 2021, small businesses are more likely to pull back on their borrowings than to increase. One in four SMEs (24.1%) will ‘throttle back’ by decreasing borrowings, with 17.6% looking to increase borrowings.

A key concern is that 40.6% of smaller SMEs (in the $1-5m revenue bracket) have no idea how they are going to fund their business for the next six months.

They are either unsure specifically how they will adapt or are unable to plan that far ahead.

Given that more than a quarter of SME respondents indicated they were covered by the stimulus, it’s important to consider what impact its withdrawal will have between now and when JobKeeper finally ends in late March 2021.

The ATO forgoing debt this year has been “another style of stimulus”, but they have signalled they will start to enforce compliance.

The financial hit for the SME sector resulting from the pandemic highlights the importance of finding the right funding to unlock working capital (see ASBFEO and ScotPac’s Business Funding Guide).

There’s an old saying “never let a crisis go to waste” and this is a message that small business owners should take seriously as there is a clear opportunity for SMEs to get ahead of the danger.

The COVID-19 crisis is a call to action for SMEs to talk to professional advisors and make the hard decisions about their business – how viable it is, what happens when ATO debts are enforced and other debts fall due, how to deal with the end of JobKeeper and making the time and effort to find the best way to fund the business.