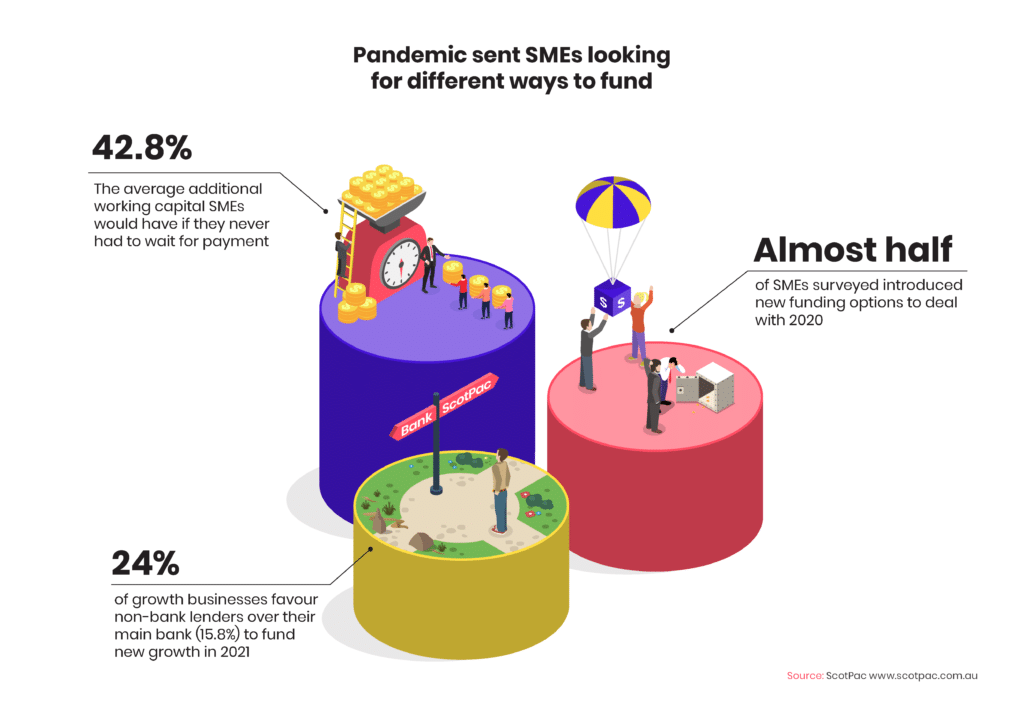

Almost half the small businesses polled in the March 2021 SME Growth Index introduced new funding options in 2020 to deal with pandemic recovery and growth opportunities.

This large cohort of small businesses (46%) looked beyond their traditional funding methods to keep operations on an even keel, while 54% were able to get by using their existing style of funding.

The most common reasons for SMEs to turn to new funding options in 2020 were:

- to develop new products and services to diversify their revenue base (31.4%)

- to buy new or replacement equipment or machinery (24.4%)

- a desire to increase cash reserves (21%)

- to refinance existing loans (20.3%)

- traditional bank funding was unable to meet their needs (15.5%)

- not enough equity in their home to fund business requirements (6.9%)

Of the one in four businesses seeking new funding methods to invest in plant, equipment and machinery, the breakdown was 10% looking for new equipment and 14.4% looking to replace old. This modest demand for investment in plant reflects ABS data indicating that capital expenditure remains relatively suppressed despite the significant expansion of the instant write-off provision.

Only 2.6% of SMEs sought new methods of funding in order to hire new staff or train existing staff.

Early payment would have massive impact

Since the Index began in 2014, small business owners have indicated regularly that delayed invoice payment terms are a critical drag on cash flow and a significant source of stress.

SMEs are waiting on average 56 days to be paid, despite recent pushes by the Federal Government and ASBFEO to reduce payment times to 30 days (East & Partners has extrapolated that this results in up to $776b being held up in late payments annually for the SME sector).

This round, we asked SMEs how much of their working capital would be freed up for the business if they never had to wait for payment.

Small businesses said they would be able to access, on average, an additional 42.8% working capital.

Estimates of the boost to working capital ranged from 11% to an astonishing high of 67.7% for some small businesses.

For smaller SMEs (those with $1m-$5m revenue) not having to wait for payment would allow them access to an extra 31.4% in working capital.

This was even more marked for larger SMEs (businesses with $5m-$20m revenue) who would gain an average 55.6% more working capital if they were paid immediately.

Young and newly launched businesses (five years or under) are feeling this cash flow crunch more severely, with on average 58.8% of working capital tied up in unpaid invoices.

Businesses over five years old estimate they would gain an additional 35.6% in working capital in an ideal world where they never had to wait for payment.

In the real world small businesses do have to wait, often too long, for payment.

So it is important for them to secure funding that smooths out cash flow gaps and allows them the confidence to take on new opportunities.

Even better if they can do so without taking on further debt or relying on using their family home as security.

Market analysts East & Partners emphasise the need for small businesses to be properly funded in order for the sector to fully recover in 2021.

New ASBFEO head Bruce Billson, and RBA assistant governor Chris Kent, have both publicly stressed the importance of small business access to finance in recent months.

How SMEs will fund 2021 growth

Small businesses were asked how they intend to fund new growth in 2021.

As in previous rounds, the two main ways to fund new growth are by using their own funds (the top option for 89.1% of respondents) and by borrowing from a non-bank lender (now at a new high of 28.3%).

One in five small businesses (21.2%) will rely on new equity to fund growth.

Once again there was a decrease in the number of SMEs intending to use banks to fund new growth, despite the range of government stimulus measures linked to bank lending.

Only 16.8% of SMEs plan to fund new growth via their main bank and 12.3% plan to use other banks.

When only growth company responses are considered, one in four growth businesses (24%) intend to borrow from non-banks to fund new growth, 15.8% will turn to their main bank and 13.1% will borrow from another bank.

The RBA has noted that while business confidence has improved markedly, many smaller businesses remain reluctant to take out new loans.

This reluctance may indicate that business owners recognise it is not an optimal solution to simply add more debt onto already over-leveraged balance sheets.

One negative flow-on effect from this reluctance to take on new debt from traditional banking sources is that many businesses have simply “kicked the can further down the road” instead of sourcing more appropriate business funding solutions, according to East & Partners.

SMEs and their advisers are encouraged to download this free Business Funding Guide created by ASBFEO and ScotPac to outline styles of funding that might suit their business.

The guide aims to educate small businesses and their trusted advisers (such as accountants, brokers and bookkeepers) about a wide range of funding options for different business situations.